It has been a month since our last update and, quite frankly, not much has changed. As the markets flirt with all-time highs and a potential shift in Fed policy, earnings season has not altered the fact that the level of investor uncertainty feels elevated. Throw in the case of a really bad winter, a geopolitical environment that rhymes with events just prior to World War I, and poor trading volumes, and it all suggests that heightened levels of unease remain. (View a printable version of this Economic Update: Mixed Signals and the Road Less Traveled)

During times of elevated uncertainty, it can help to stay focused on what we know and what we can control rather than what we don’t know and can’t control. So let’s get started.

Engineering teams often like to “reverse engineer” the products of their competitors to get an understanding of how they are made, what they cost, and where their own products may excel or fall behind. In our business, we often like to reverse engineer the state of the economy by unpacking what the latest market action may be telling us rather than economic releases or earnings reports of their own accord.

While this approach clearly has its flaws – one wag once said that the stock market correctly predicted 10 of the last 2 recessions – it does help to get a sense for where market expectations may be trending and therefore where surprises may be most aptly rewarded or punished. While the financial markets may not provide the most accurate of economic forecasts, they probably do a decent job of telling the story of the average forecast, if that makes any sense.

Right now, the bond and stock markets are providing a lot of unusual mixed signals. While the stock market is near all-time highs and the earnings season – proforma of weather related effects – has been solid, the bond market has been telling an alternative story. Bond yields, which often move in the direction of the economy, fell to 2.53% on Wednesday, suggesting lurking weakness and potential unease. Classically speaking, yields move down when economic growth slows in real terms. The bond market doesn’t appear to agree with the Fed’s more bullish outlook, economists’ calls for a weather related snapback, and generally improving employment payrolls.

The Fed is still buying bonds, but less than it had been buying. In spite of “tapering” its purchases, the overall demand for US bonds has been growing faster than the supply, forcing rates lower and suggesting that a majority of fixed income investors aren’t as positive about the outlook as the Fed may be, at least in the short run. Of course, U.S. bonds are one of our countries most significant exports, valued as a source of stability and liquidity around the globe. It may be that a decline in our rates may not reflect concerns about our own economy, but a powerful subset of foreign investors more worried about their own.

Initial first quarter GDP readings were indeed abysmal at just slightly greater than zero, but nearly every economist we know, and the Fed, believes that the weakness was largely due to extraordinarily poor weather in the United States this winter. Recent regional purchasing manager indices, commentary accompanying first quarter earnings, and employment statistics all appear to affirm the temporary nature of the weather related setbacks apparent in the GDP release.

As longer term stock market investors, the key question for us isn’t so much whether or not there is a snapback in demand following a few months of weather induced shrinkage, but whether or not that snapback in demand sustains itself into the future. The bond market and even the internal actions of the stock market appear to be questioning this assumption.

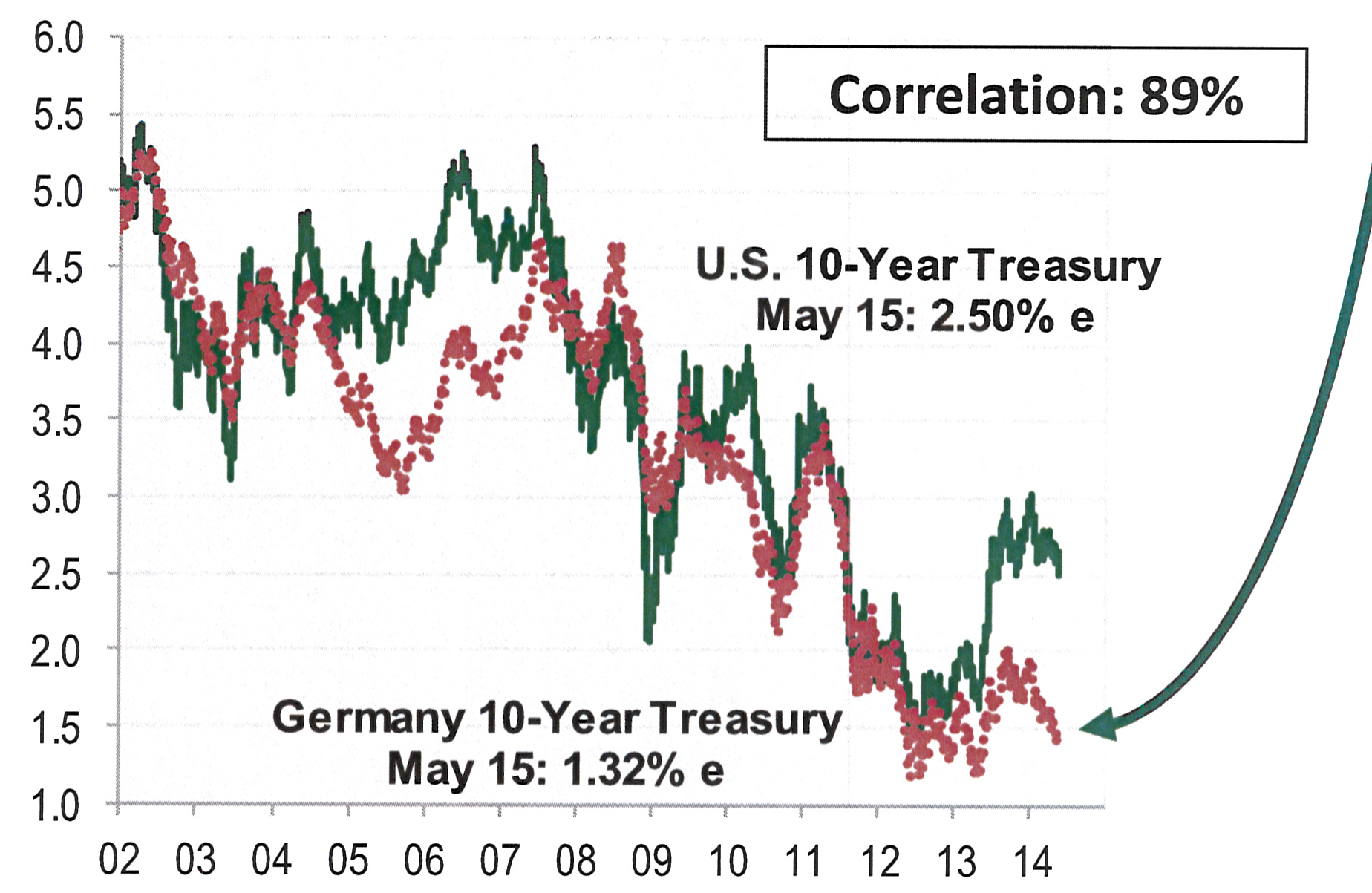

On the other hand, the bond market could be telling us that the problem isn’t within the domestic market but international markets. I was surprised to hear that German 10 Year bonds have lower yields compared to US bonds – nearly half as much at 1.3% versus 2.5%. (Graph: Cornerstone Macro) While our economy may be growing faster than Europe’s, their yields may be declining in the face of anticipated easing by the ECB later this year. Downward pressure on our rates may be more of a function of the unease and chase for yield by foreign investors worried about their own economies than ours. Even with the potential currency conversion risks, twice the yield might be more than compensating, attracting unusual demand for US bonds.

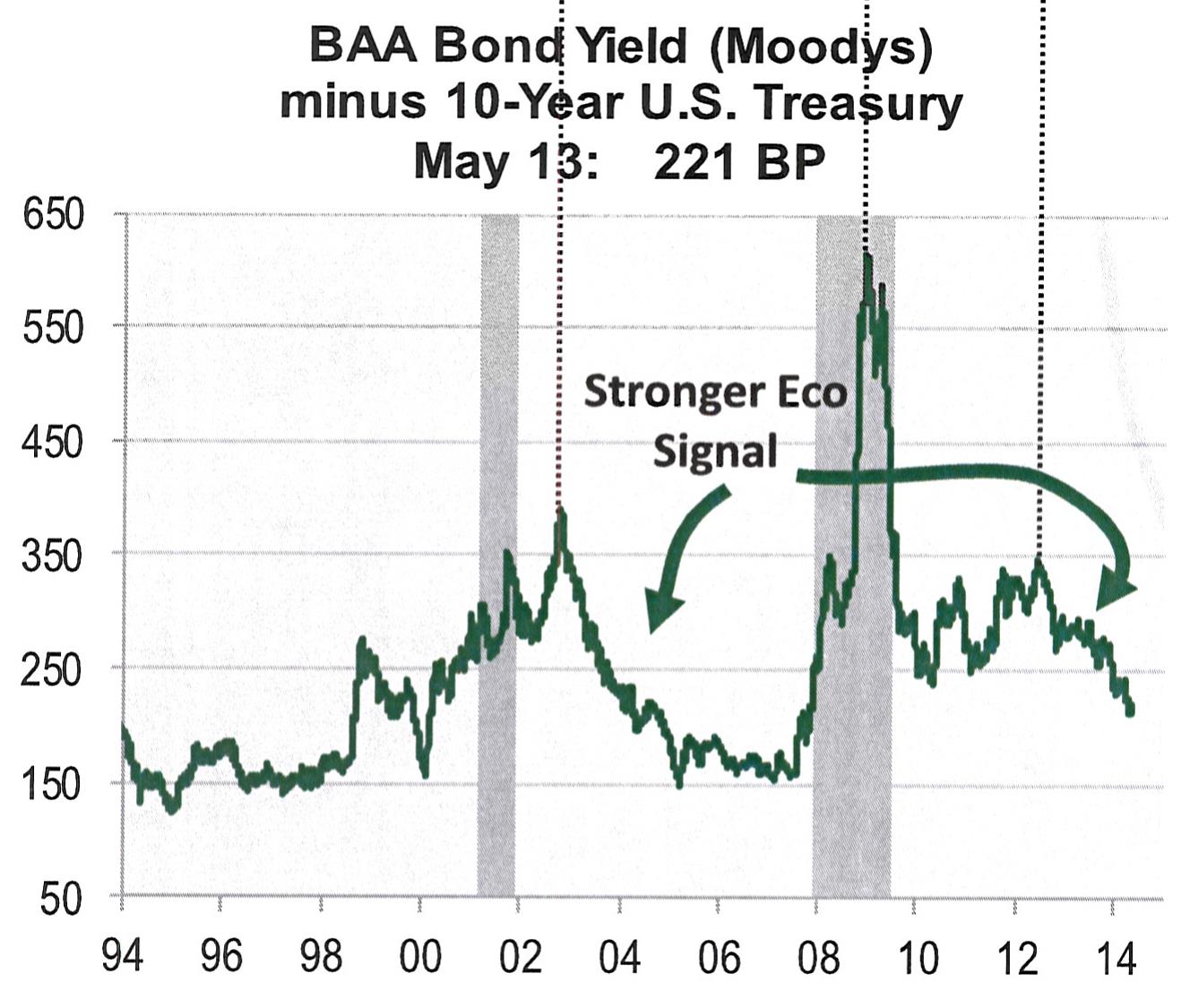

Another data point which could suggest that the source of concern may be international in nature is the direction of yield spreads. Typically yield spreads – or the difference in yields between high quality and lower quality bonds – move opposite to the direction of the economy. In other words, if the economy is worsening, investors usually require more yield to buy lower quality issues, not less yield as is the case today. While 10 Year treasury yields are declining, spreads are also declining, suggesting that the outlook for the economy among bond investors may be improving rather than deteriorating. (Chart: Cornerstone Macro)

As the default currency in a global economy, it is increasingly likely that the monetary policy actions of foreign central banks will have a far greater impact on our domestic rates than used to be the case, just as our own QE efforts in the past three years had an unusual impact on many emerging markets.

While retail sales results were generally lackluster for all but the best of retailers this earnings season, most investors were willing to accept the weather related excuse as temporary in nature. Wednesday night, however, Walmart may have spooked investors when it not only missed top and bottom line expectations by a sizeable margin but also guided expectations down for the coming quarter, suggesting at least for its demographic that the case for a a quick snapback may be overstated. What do we think? Personally, we think Walmart’s results have been under pressure for a while now, not simply because the economy has been punk, but because superior, higher service, lower cost models from the likes of Costco and Amazon may be taking share.

So, if our economy is improving or at least not deteriorating, what could be the source of international unease? Obviously geopolitical concerns remain, including Ukraine’s upcoming elections and the renewed unease in Turkey following its mining disaster. China, as well, continues to experience a painful slowdown in growth, with clearer signs that its real estate bubbles in housing and commercial construction may be nearing an end. All of this weakness and uncertainty around the globe could be colliding with the notion among domestic economists and the Fed of a generally improving US outlook. Oddly, we could be moving into the best of all worlds where our economy continues to grow at a moderate pace and interest rates remain low, even as Fed policy is normalized, thanks to slower growth expectations in overseas economies. Classically speaking, a low inflation, low growth environment is the best of all worlds for the stock market.

So, summing things up, what do we know? Interest rates in the United States have been falling even as domestic economic data points continue to improve and earnings results remain positive. In our book, this is likely a function of greater concerns about growth in international markets than our own. Second, the corporate earnings season, in spite of Wednesday night’s results from Walmart, remains robust. According to our work, the average year over year revenue and earnings growth rate for first quarter holdings in the Broadleaf Growth Equity Portfolio were 24% and 34%, respectively, hardly signs of a troubled environment. In fact, these results represent an acceleration in growth from the fourth quarter rates of 21% and 27% respectively, in spite of the bad Q1 weather.

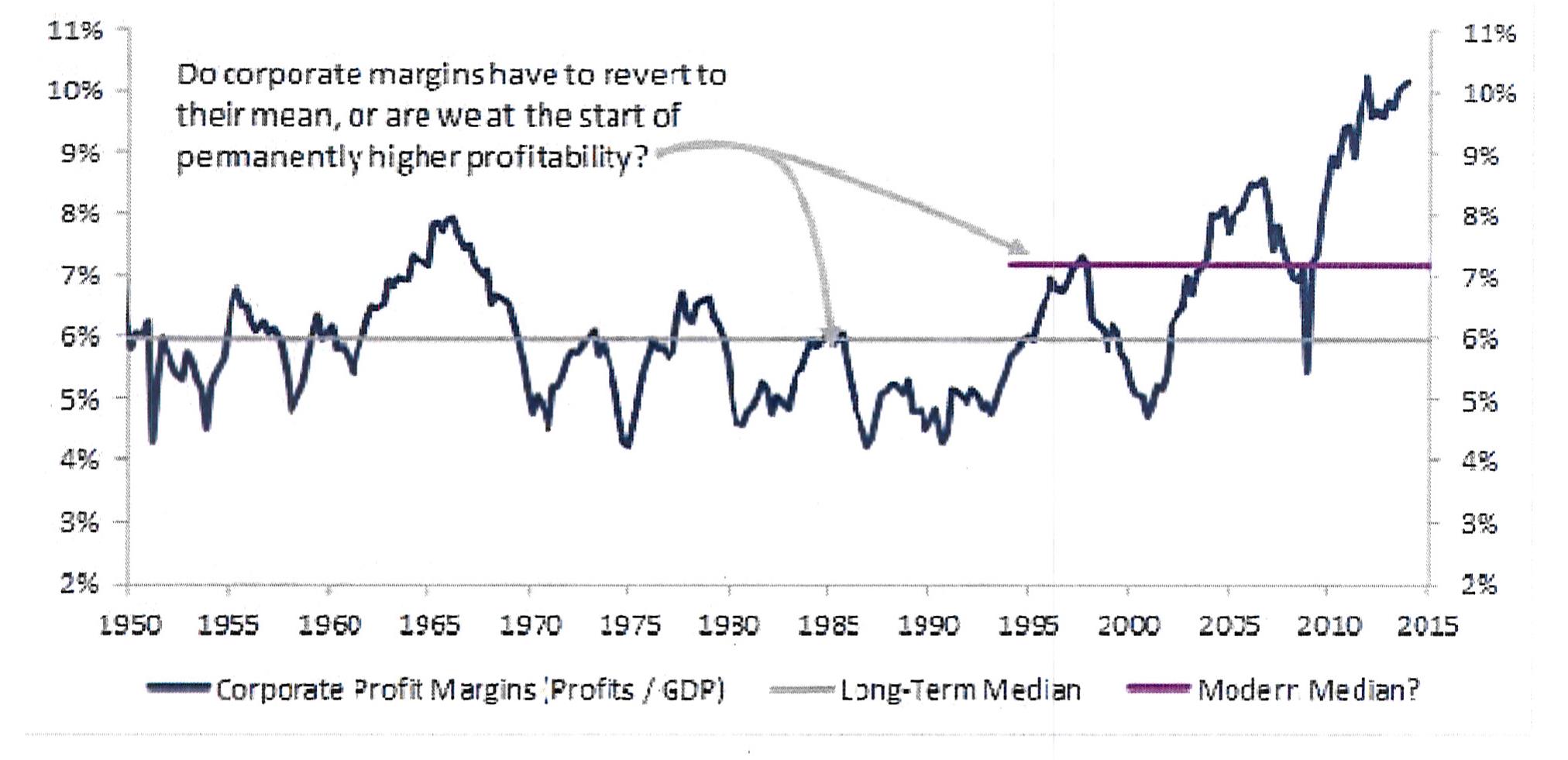

As the following chart from ISI Group shows, corporate profitability is clearly in new territory, causing some to expect an impending reversion to the mean, a bear case that gets more press given the bond market conundrum. But rising corporate margins have been trending higher since 1995, about the time Netscape Navigator and Internet Explorer were introduced to the world as two of the internet’s first killer apps. New apps continue to drive productivity higher today, affecting the structure of many existing industries and giving birth to new ones entirely. While China has certainly played a role in keeping labor costs constrained, I suspect technology has been just as important, if not more important.

Fortunately, the single factor which is most correlated to stock price performance over the long run isn’t interest rates, fed policy, inflation, or yield spreads but earnings. Even though financial assets reprice when interest rates move up – and again rates aren’t moving up yet, they are moving down – earnings growth over time dominates the value creation process. While I fully expect high growth stocks to experience a larger valuation reset in anticipation of rate increases than most areas of the market – and perhaps we’ve already started that process – I also fully expect this group of stocks to enjoy the greatest rate of earnings growth over the next five to ten years regardless of what the Fed does or doesn’t do at its next few meetings. I do not believe that growth stocks are so overvalued at this point to preclude superior returns down the road.

Historically speaking, the best growth companies tend to be immune to the ebb and flow of the economic cycle in all its stages but recessions, in which case, because of their generally higher valuations, they are usually hit the hardest even though their earnings hold up better than most. In spite of the action in the bond market and the questionable earnings reports from folks like Walmart, we do not anticipate the economy entering into a recession anytime soon. In fact, as we stated earlier, Walmart’s issues, longer term, are likely less due to the weather and the economy than the onslaught of the low cost structure ecommerce crowd, in particular Amazon, but also Costco.

Just as you can never underestimate the economic cycle’s impact on the stock market, it is important to recognize the impact that innovation can have on the old way of doing things. While growth managers, including ourselves, typically make mistakes by overpaying for future earnings growth that isn’t sustainable, value managers often make mistakes by overpaying for historical levels of earnings that aren’t sustainable.

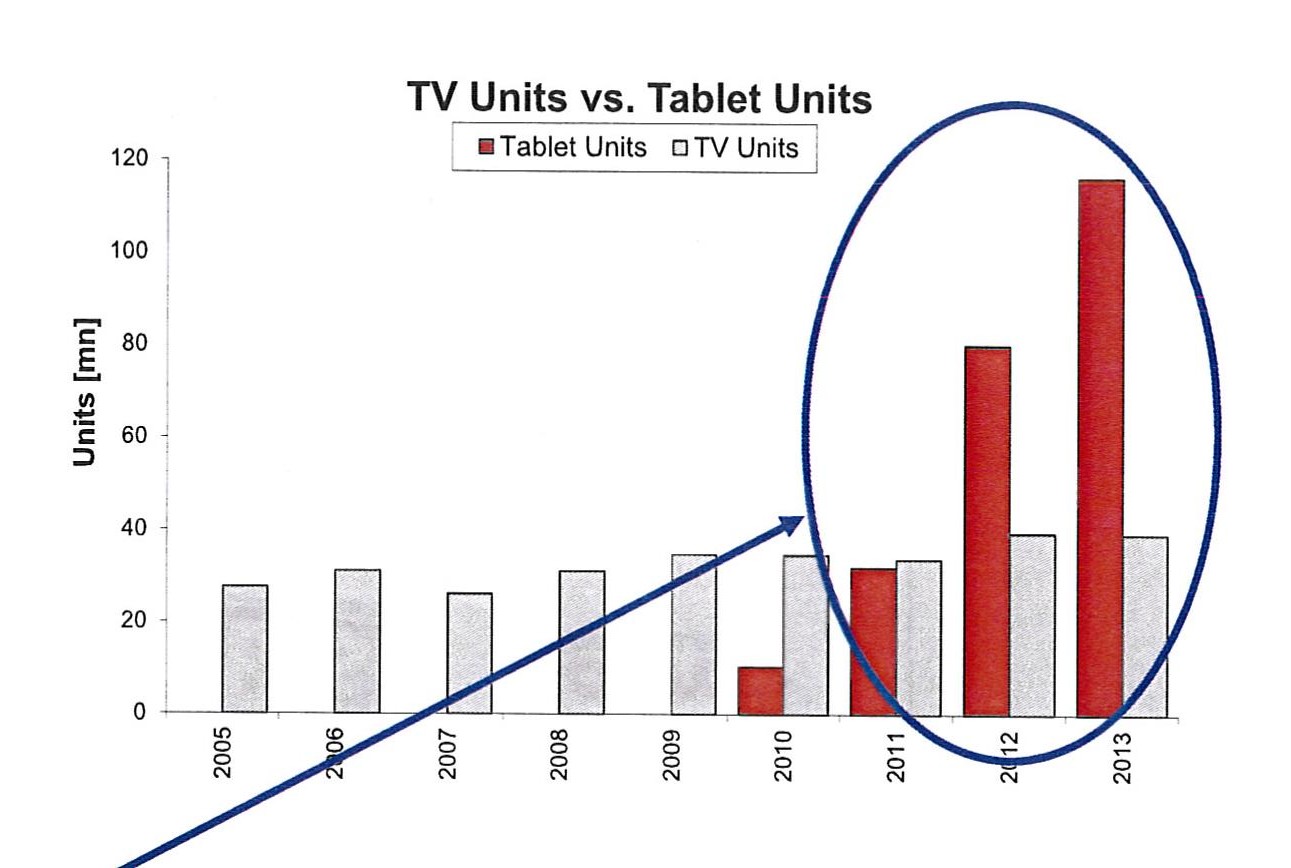

The rise of new advertising models from Google and Facebook at the expense of traditional mediums like newspapers, magazines and the radio continues. As the graph below shows (ISI Group), tablet unit sales exceeded television sales for the first time in 2012. This may be a reason traditional media companies are in the process of consolidating. Not only are new media companies taking an increased share of the advertising pie, but they are also starting to produce their own content and deliver it via methods increasingly popular to future generations. While shifts in Fed policy and interest rates may cause a valuation reset for high growth stocks in the short run, it is doubtful that it will derail the long run earnings trajectory occurring in a whole host of industries affected by the dawn of the internet, now thirty or so years young.

We’re not absolutely convinced that the bounceback we’re seeing in some economic indicators is much more than a snapback from depressed Q1 weather related demand. If that is indeed the case, then interest rates could continue to remain lower for an extended period of time. While our economy may be expanding, a new normal rate of growth for an extended period of time following a severe credit induced recession would not be unprecedented, but in fact, likely. As we said before, slower growth and lower inflation/interest rates are among the very best economic environments for stocks. Companies that sustainably grow earnings faster than most not only benefit from higher levels of future earnings, but also the higher multiples placed by the market on a given dollar of earnings.

While merger and acquisition related activity has been improving in recent months, company management teams appear to be far more focused on stock buybacks and dividend increases as a way to create shareholder value. While this may be appropriate for mature companies in mature industries with slowly declining addressable markets, it would be a mistaken strategy for high growth markets where the industry value has not yet been achieved or determined.

In recent days, we have been comparing the financial statements of such newcomers as Amazon, Salesforce and Under Armour to their counterparts like Walmart, Oracle, and Nike in their go-go glory days. While today’s class of company is indeed more expensive than its brethren were in their day and age at similar sizes, what struck us as most interesting from the analysis was a complete lack of emphasis on free cash flow from the 1985-1995 financial statements. While cash generation has always been important, the concept of free cash flow was something you had to compute fifteen years ago, while today it’s typically a focus of almost any earnings call.

The obsession with free cash flow isn’t necessarily a bad thing, but it may also be a fad whose day of emphasis may at some point come to an end. Free cash flow, or cash from operations after capital expenditures, is a number that can be manipulated by simply underinvesting in one’s company over time. At some level, particularly for more mature companies, this may make sense, but for companies that want to last for generations, they must be willing to engage in maintenance spending and occasionally, to entirely reinvent themselves. The notion that all companies should cease taking new entrepreneurial risks simply because they are public in an environment where share buybacks and dividend increases are far more stylish to value creation is shortsighted.

It would be a mistake to suggest that there are no companies that could benefit from greater financial discipline just as it would be a mistake to suggest so few could benefit by taking new entrepreneurial risks with existing shareholder capital. If no one had ever taken a risk on spending capital on a new venture, there would be no operations capable of generating cash for stock buybacks and dividends today.

As always, balance is key, but perhaps we’ve traveled the conservative path for too long and the greater dividends could accrue to future investors by taking the road less traveled.

Kindest regards,

Doug MacKay, CEO & CIO

Bill Hoover, President

Mike Czekaj, Research Analyst